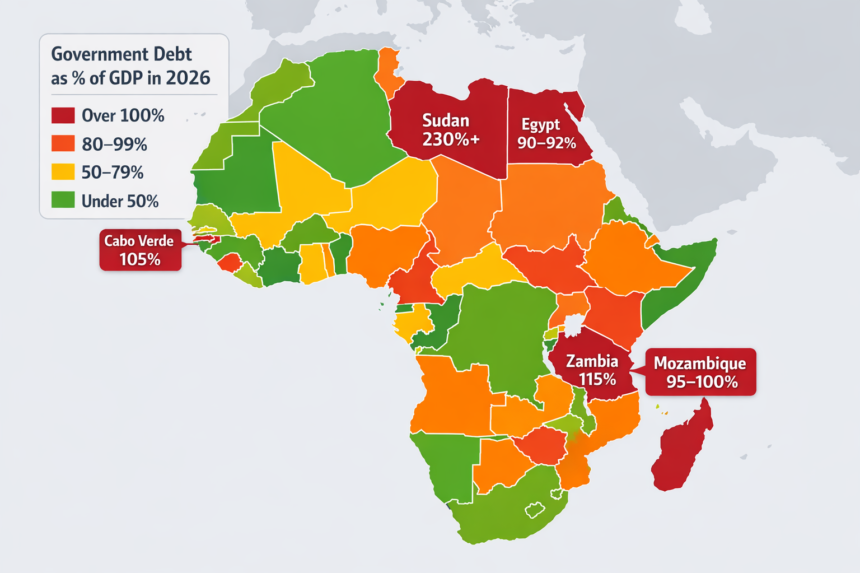

The narrative that Africa faces a persistent debt crisis has become entrenched. In fact, despite representing nearly one-fifth of the world’s population, the continent accounts for less than 3 percent of global sovereign debt. Moreover, Africa’s average debt-to-gross domestic product ratio, at 67 percent, is markedly lower than those of Europe (88.5 percent), the US (122.6 percent) and Japan (236.7 percent).

Nonetheless, many countries on the leastindebted and most capital-starved continent remain stuck in a debt trap. Senegal is this week hosting an international conference to address the country’s escalating debt crisis and, crucially, one of its main drivers: the structural asymmetries embedded in the global financial system.

This flawed architecture has obstructed Africa’s access to affordable, long-term capital and prevented the continent from diversifying its sources of economic growth and trade, transforming debt from a manageable development instrument into a self-perpetuating cycle of vulnerability. Credit ratings agencies such as S&P,

More Read

Fitch and Moody’s deepen the debt trap by assigning most African countries lower ratings, which substantially elevate their borrowing costs and limit their market access. Sovereign bonds issued by African countries typically yield 8 percent to 15 percent, in sharp contrast to yields of 1 percent to 5 percent in Europe and North America.

These spreads impose high macroeconomic costs. In short, Africa is paying so much not because of the amount of debt it has accumulated, but because of how that debt is structured and perceived. For African countries, it costs more to borrow less, setting unrealistic return on investment expectations that further undermine debt sustainability.

As a result, a growing number of African countries have pursued rollovers and refinancing options, such as issuing new eurobonds, to settle maturing obligations — falling deeper into the debt trap. This has accelerated the shift in recent decades from long-term concessional loans to short-term commercial debt.

Private creditors now hold more than 40 percent of Africa’s external public debt, up from 17 percent in 2000. Loans with shorter maturities compress repayment timelines, increase refinancing risks and are misaligned with Africa’s long-term development objectives. They also raise the risk of maturity clustering.

Moreover, the erosion of human capital and a chronic infrastructure deficit in an austerity-prone operating environment leave many African economies vulnerable to commodity shocks that drive external liabilities higher. When balance of payments crises invariably materialize, African governments are compelled to borrow in foreign currencies and implement adjustment programs that prioritize short-term fiscal consolidation over longterm development.

These programs’ procyclical austerity measures can help stabilize public finances but often weaken state capacity and lower potential economic growth. Over time, this leads to repeated cycles of borrowing, crisis and adjustment — the very definition of a debt trap. To break the cycle of dependency and accelerate development, policymakers must redesign the global financial architecture.

Aligning debt maturities with longer-term development objectives requires improving access to concessional financing, which can be achieved by strengthening development finance institutions’ capital base. At the regional level, policymakers must fast-track monetary integration and the development of deeper domestic capital markets to support long-term borrowing in local currencies and address structural mismatches between currency denomination and revenue generation.

It is also crucial to reform credit ratings agencies’ methodologies to achieve parity in access to affordable development finance and to reduce the incidence of procyclical policies. This will not only rebuild these institutions’ credibility but also foster economic growth and sustainable development. Lastly, the international community should regard fiscal consolidation and debt sustainability as being in service of a broader goal: to promote Africa’s economic development.

Africa is not heavily indebted — it is a victim of deep-seated inequalities, underpinned by an international financial architecture that prevents structural economic transformation and perpetuates debt crises. If the world is to harness Africa’s demographic dividends and unlock its growth potential, both of which are essential to maintaining financial stability worldwide, the institutions, rules and norms of global governance must become more balanced and development-oriented.

To break the cycle of dependency and accelerate development, policymakers must redesign the global financial architecture.

Source: ARAB NEWS